MMS • RSS

Posted on mongodb google news. Visit mongodb google news

cemagraphics

MongoDB’s (NASDAQ:MDB) stock remains near recent lows, despite rapidly easing inflation and continued strong performance. Management has guided to a significant slowdown in growth going forward as macro pressures mount, but it is not clear how conservative this guidance is. For investors with a long-term horizon, MongoDB appears attractively priced given the company’s potential.

According to IDC, the 2022 database market is 84 billion USD and expected to grow to 138 billion USD in 2026. MongoDB’s share of this market is still only in the low single digits, providing a large growth runway. Much of this market is locked into legacy databases though, with only new applications and a small percentage of existing applications up for grabs.

MongoDB’s document model allows them to address much of this market and is likely an attractive option in the current environment, as it allows customers to simplify their tech stack and reduce costs. Amongst functionality that MongoDB has added in recent years, customers are consolidating search workloads on top of MongoDB and there is also a lot of interest in using MongoDB for time series data. Time series data enables customers to automate decision making into their applications.

Despite MongoDB’s long-term potential, the current environment is difficult for most software companies, although MongoDB appears to be facing a somewhat different set of issues. MongoDB continues to win new customers and unlike many peers hasn’t seen an increase in deal cycles or extra scrutiny on deals. Headwinds have primarily been related to consumption, which is dependent on usage of applications that are built on top of MongoDB’s database.

From a competition perspective MongoDB is well placed, as companies today are driving competitive advantage on the basis of their internally built technology. MongoDB offers a platform that allows customers to innovate more quickly and scale their business and this is generally the reason that customers pick MongoDB, rather than on a cost basis.

There has not been any fundamental change in the competitive landscape in recent years and MongoDB’s win rates remain exceptionally high against a range of competitors. Management has stated that their primary issue is ensuring they are involved in all potential opportunities given the relatively small size of their salesforce.

Financial Analysis

A number of customer segments that were below expectations in Q2 bounced back in Q3, particularly the mid-market channel globally and MongoDB’s enterprise business in Europe. Enterprise Advanced also continues to exceed expectations, which is notable given the requirement of an upfront commitment. Enterprise Advanced is a self-managed version of MongoDB, which many customers are using as an on ramp to the public cloud.

Atlas revenue grew 61% YoY in the third quarter and now represents 63% of revenue. Atlas consumption improved in Q3 relative to Q2 but still remains below historical levels. Digital native customers remain a problem from a consumption perspective though. These customers are generally part of MongoDB’s mid-market segment, which constitutes a mid-teen percentage of MongoDB’s revenue. Digital native companies are a minority, but a significant minority of the mid-market segment.

Revenue in the fourth quarter is expected to be approximately 335 million USD, which would be a substantial deceleration in growth, although it is unclear how conservative this guidance is. Slower sequential Atlas consumption growth is expected in the fourth quarter and Enterprise Advanced sales are also not expected to be as strong.

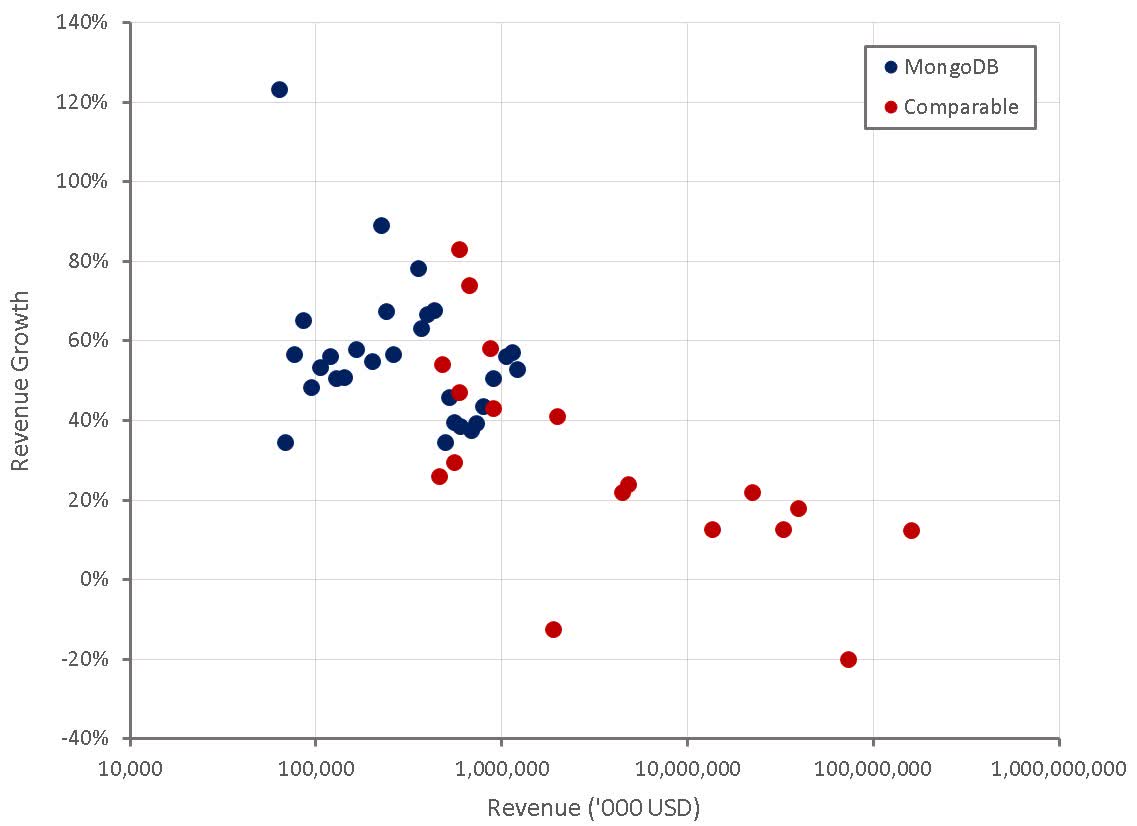

Figure 1: MongoDB Revenue Growth (source: Created by author using data from company reports)

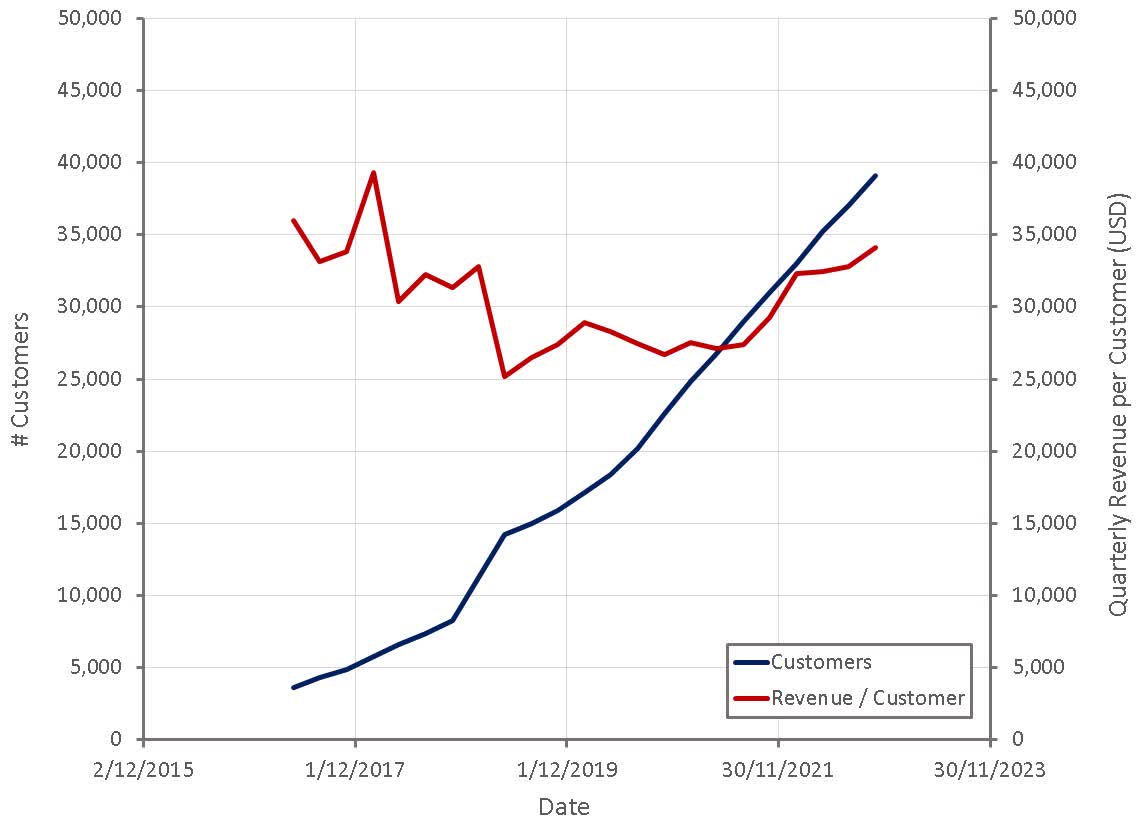

MongoDB added 2,100 customers in the quarter, of which 500 were direct sales customers. Growth in MongoDB’s customer count appears linear though, which will weigh on growth rates in time, but is currently being offset by increasing revenue per customer. The growth in total customer count is being driven primarily by Atlas which had over 37,600 customers at the end of the quarter compared to over 29,500 in the year ago period. The vast majority of MongoDB’s growth comes from existing workloads, as Atlas workloads tend to start small. Continued growth in the customer base remains an important driver of long-term growth though.

Of the total customer count, over 5,900 are direct sales customers, which compares to over 3,900 in the year ago period, demonstrating the growing importance of MongoDB to larger customers. MongoDB’s net ARR expansion rate remains above 120%, and MongoDB now has 1,545 customers with at least 100,000 USD in ARR, up from 1,201 12 months ago.

Figure 2: MongoDB Customers (source: Created by author using data from MongoDB)

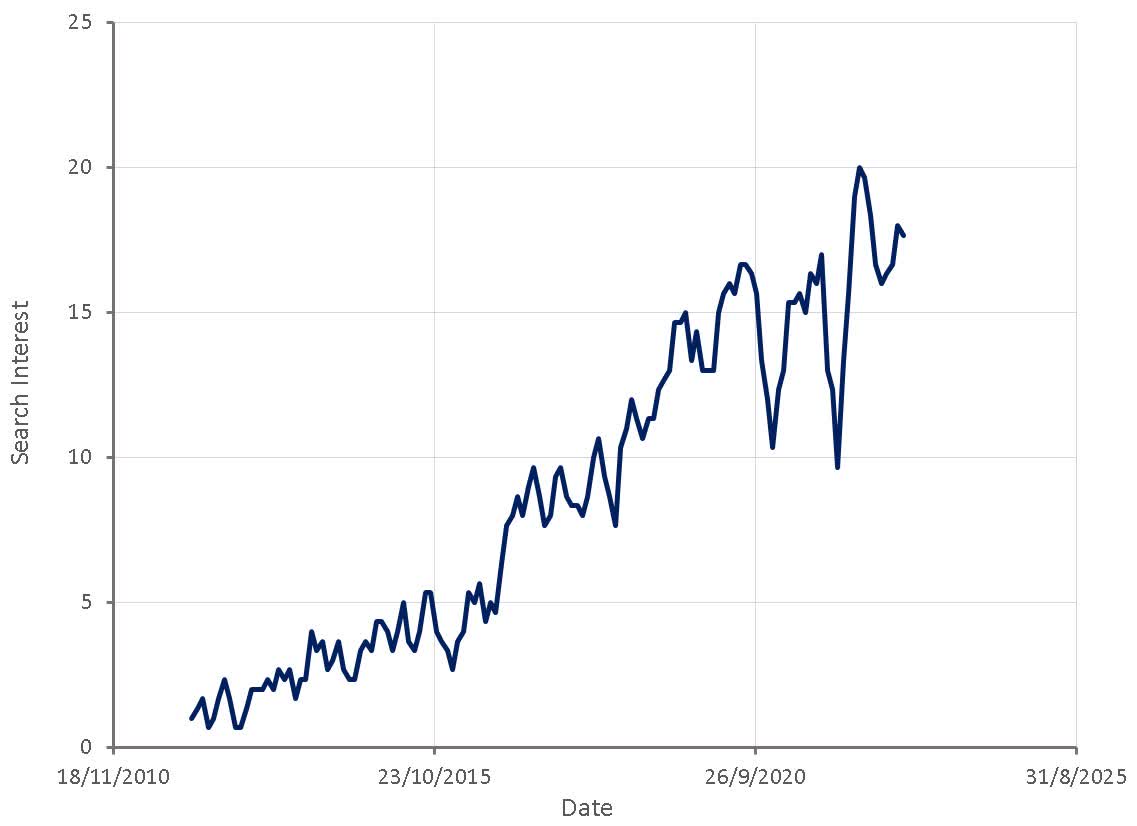

Upstream indicators of demand generally appear to be reasonably strong. In the last 12 months MongoDB’s open-source community server has been downloaded more than 115 million times from their website. Search interest for MongoDB pricing also continues to increase and in the third quarter there were over 300,000 sign-ups for the Atlas free tier, up 15x over the last five years.

Figure 3: “MongoDB Pricing” Search Interest (source: Created by author using data from Google Trends)

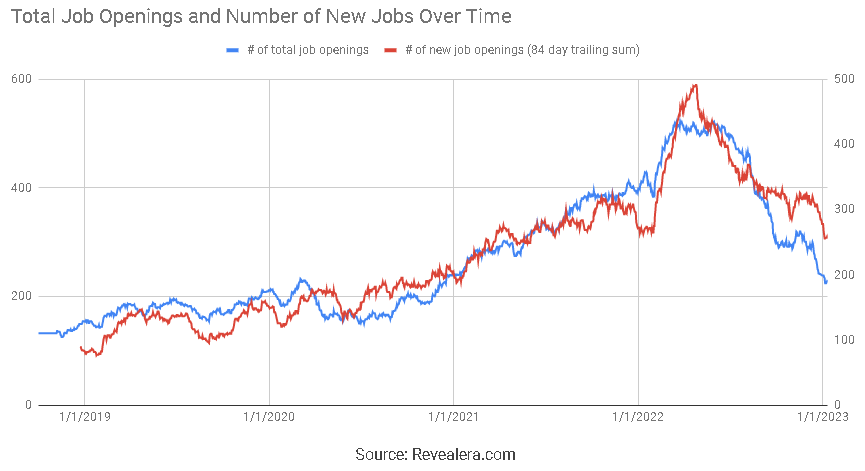

Job openings mentioning MongoDB began easing in August and this accelerated in December, a potential indicator of weaker growth going forward.

Figure 4: Job Openings Mentioning MongoDB in the Job Requirements (source: Revealera.com)

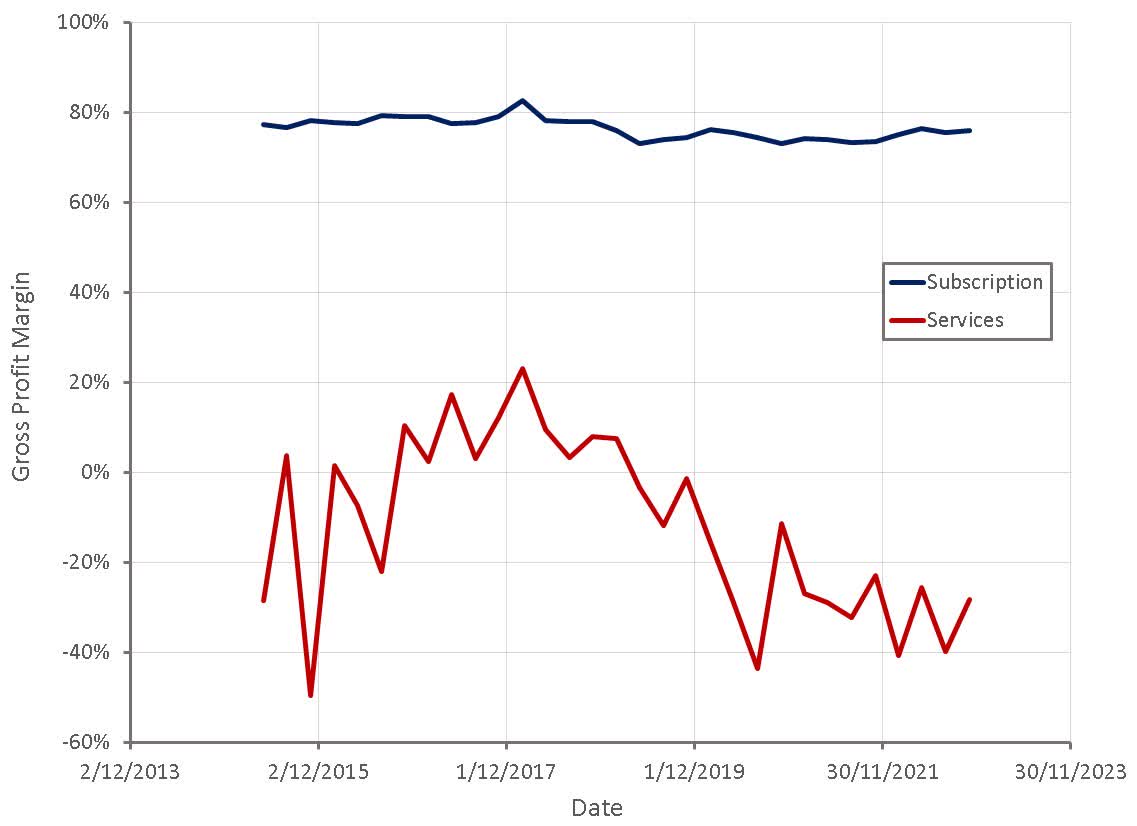

Figure 5: MongoDB Gross Profit Margins (source: Created by author using data from MongoDB)

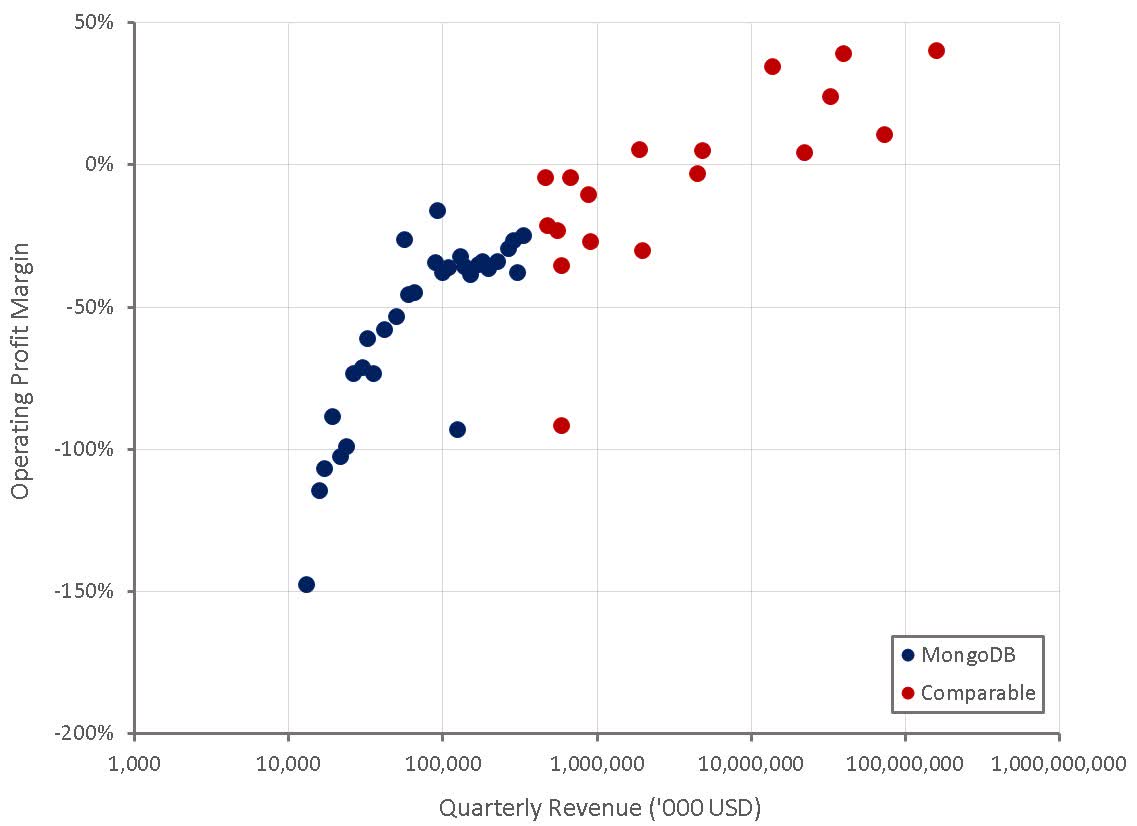

MongoDB’s operating profit margins continue to improve, more or less in line with what should be expected. Sales and marketing expenses continue to dominate MongoDB’s operating expenses, and have been fairly constant relative to revenue over the past few years. This is not particularly concerning given that MongoDB has high win rates against competitors and low churn. It is also reflective of the fact that MongoDB is building out a direct sales force.

A number of large systems integrators are in the process of setting up business units focused on MongoDB given the size of the growing MongoDB practice. MongoDB currently has close to 200 ISVs co-selling relationships, which is up more than 2x compared to two years ago.

Figure 6: MongoDB Operating Profit Margins (source: Created by author using data from company reports)

MongoDB’s pace of hiring has slowed significantly over the past 12 months, with particularly large declines in September and December. This could indicate an expectation by management of lower growth going forward, but is likely at least in part due to an increased focus on profitability.

Figure 7: MongoDB Job Openings (source: Revealera.com)

Valuation

MongoDB currently trades on a near record low revenue multiple, which makes the stock appear attractively priced. This needs to be weighed against the uncertain macro environment, higher interest rates and current investor demand for profitability though. Given that there is far less business model uncertainty than when MongoDB traded on similar multiples in 2017/2018 and that inflation is falling rapidly, this still appears to be an attractive entry point. Based on a discounted cash flow analysis I estimate that MongoDB’s intrinsic value is approximately 300 USD per share.

Figure 8: MongoDB EV/S Multiple (source: Seeking Alpha)

Conclusion

MongoDB competes in a large market that continues to grow rapidly. Given the company’s relatively high gross margins, high win rates against competitors and low churn, the business is likely to perform well unless their competitive position changes significantly. The stock price does not currently reflect this due to an unduly large focus on the next 1-2 years, which remain uncertain.

Article originally posted on mongodb google news. Visit mongodb google news