MMS • RSS

Posted on mongodb google news. Visit mongodb google news

Certain growth stocks have underperformed recently and have done even worse after the tariff spook. These stocks are now sitting at historical lows and could be on the cusp of bottoming out, as most tech stocks have done quite well despite broader market fears.

If you have a lot of cash on hand or if you think you are overly invested in defensive stocks, it might be worth shifting some of your money into more aggressive rebound picks like these. Many of the Magnificent Seven stocks have already rebounded significantly, so looking deeper into the market is a good idea. Here are three such growth stocks to look into:

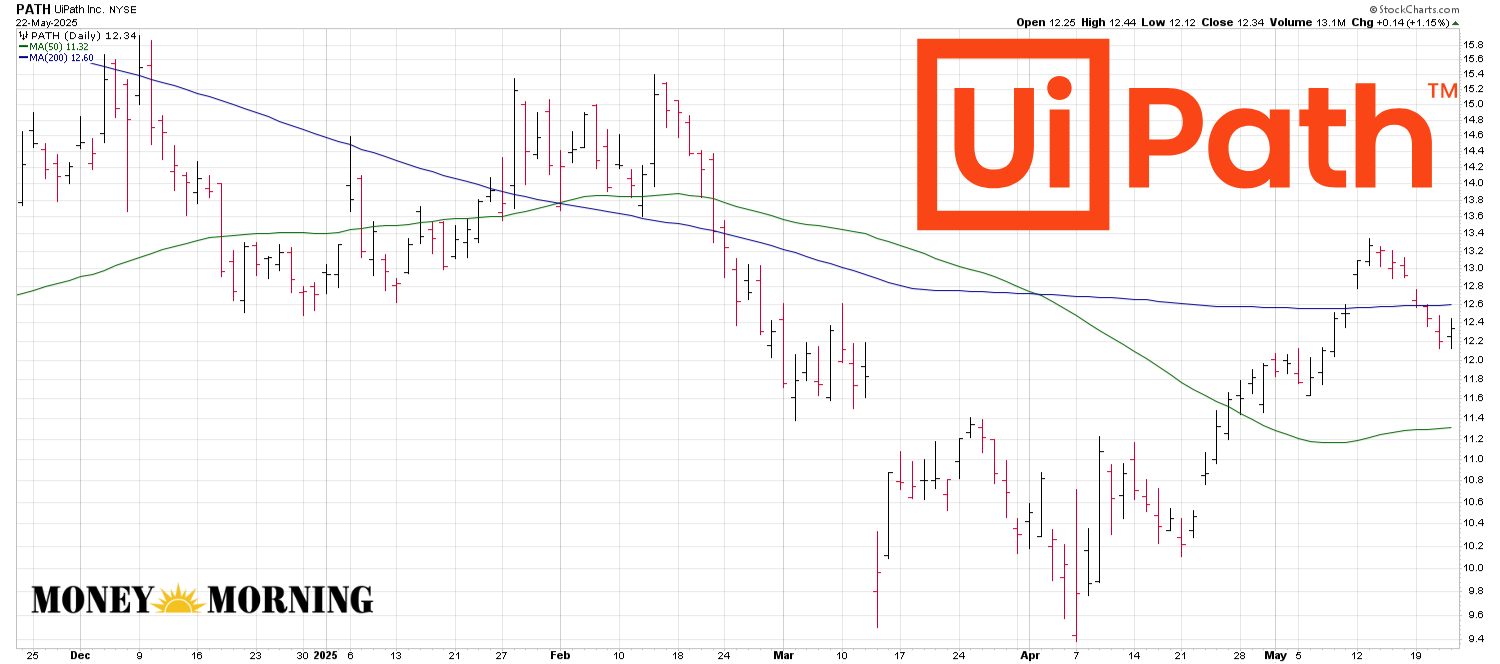

UiPath (PATH)

UiPath (NYSE:PATH) is a Robotic Process Automation (RPA) company that uses AI for robots. It is hard to automate things without software, and the progress in recent years has shown that the software part is getting increasingly more important.

I’m bullish on this company because eventually, the white-collar AI boom will spill into the blue-collar sector as well, if it hasn’t already. Companies are increasingly using automation whenever possible and are trying to increase long-term margins through robotics.

UiPath is well-positioned to benefit from this megatrend. The company is one of the biggest suppliers of software to robotics companies, and any growth in that sector will translate into more growth and profits here.

UiPath also recently turned profitable, and it has $1.63 billion in cash with very little debt. The stock is trading at a 23 times earnings multiple, whereas investors have paid around 39 times earnings historically.

Cognex (CGNX)

Cognext (NASDAQ:CGNX) is a similar bet to UiPath. It is a provider of machine vision products. The company’s products can allow robots and machines to “see” and interpret visual information. In turn, this can be used for industrial automation.

CGNX stock is down 49.3% from its high in 2023 due to a cyclical slowdown in the consumer electronics and semiconductor markets, as the EV market weakened. Currently, the bulk of its orders come from the automotive, consumer electronics, and logistics sectors. The automotive sector saw a decline due to high interest rates lingering around, whereas consumer electronics have been historically cyclical.

It is now broadening its reach significantly and focusing on factory automation and AI-powered machine vision software.

The stock could rebound significantly as its financials are picking up. EPS is expected to grow 31.6% this year and 29.6% next year. Revenue is also expected to grow 4.3% this year and accelerate to 10.4% next year.

The PE ratio at 44 does look expensive, but earnings could expand massively, especially as rates are cut. The company could see a massive ramp-up in orders as interest rates are eventually cut and consumers become more open to buying expensive EVs.

MongoDB (MDB)

MongoDB (NASDAQ:MDB) is a popular NoSQL document-oriented database. It stores data in JSON-like documents with dynamic schemas and is used in a variety of modern apps.

This is a high-margin company that went off course recently after it issued softer-than-expected guidance for its FY2026, which began in February this year. Both EPS and revenue were guided lower, and there are concerns over the growth of its Atlas cloud-based database service.

Businesses worldwide are aggressively moving their applications and infrastructure to the cloud. MongoDB Atlas, its fully managed cloud database service, is perfectly positioned to capture this demand. Many companies are still running on outdated relational databases. The sheer amount of data being generated is staggering and continues to grow exponentially, and MongoDB’s document structure has a lot of flexibility when handling data and is very popular for that reason.

I believe it’s a good time to buy the dip since a major inflection just happened. MongoDB has long been a loss-making company, but it just reported its first positive net income in the most latest quarter and almost completely eliminated its debt. It now holds $2.4 billion in cash.

Software companies with double-digit EPS and sales growth that can be sustained often trade well beyond 10x forward sales to around 15-20x as they improve margins. It’s a SaaS company on its way to doing just that as it starts making profits, so I think it’s a good time to buy the dip for the long run.

MDB stock has historically traded at 18x sales, even without profits. It currently trades at just 7x sales.

More Trending Stories from Money Morning

Article originally posted on mongodb google news. Visit mongodb google news