MMS • RSS

MongoDB has helped to fundamentally change databases, but will that unseat Oracle?

Oracle (ORCL 0.40%) first introduced its relational database (the one that can be visualized in tables of rows and columns) in the late 1970s.

While the Oracle database served user needs for decades, the nature of data has changed as computing capabilities have increased. That need prompted MongoDB (MDB -1.72%) to introduce Atlas, a non-relational database that can store unstructured data types.

However, Oracle responded by introducing its own non-relational database. It has also pivoted into the fast-growing cloud infrastructure business. Does this response mean that Oracle is still a better software-as-a-service (SaaS) stock for investors, or should they buy MongoDB as it spearheads a major shift in the industry?

The case for Oracle

Given Oracle’s longtime presence in the tech industry, it is the more stable stock of the two. As the world’s largest database management company, it has long served customers and shareholders with various IT services.

The company derives most of its revenue from its cloud services and license support segment. This includes its database services, applications such as its e-business suite and PeopleSoft enterprise, and its cloud infrastructure services.

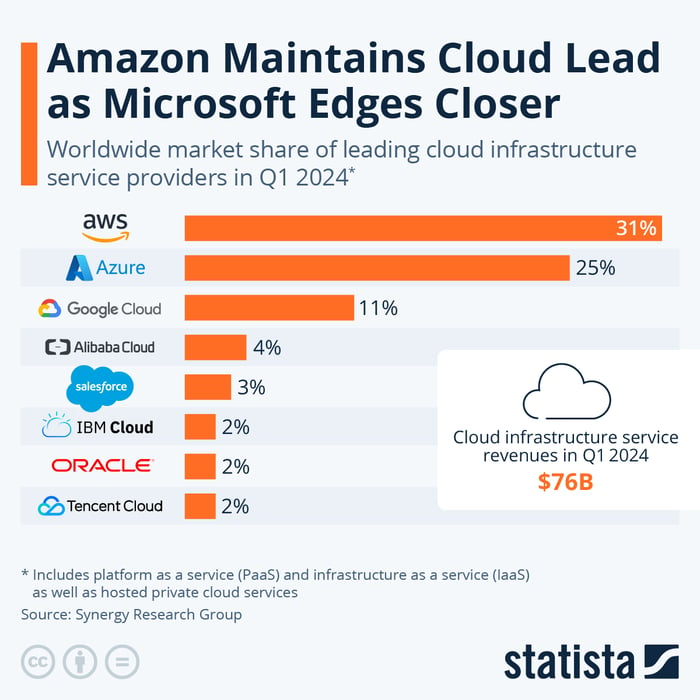

While not among the largest cloud companies, it holds about 2% of the cloud market share, according to Statista. Since cloud computing plays a critical role in supporting artificial intelligence (AI), Oracle is unlikely to go into decline and could leverage AI to keep it relevant in the database market.

Image source: Statista.

In the first quarter of fiscal 2025 (ended Aug. 31), revenue of $13 billion rose 6% from year-ago levels. This matched the revenue growth rate for fiscal 2024, which was also 6%. Still, because it limited operating expense growth to under 2%, Oracle reported $2.9 billion in net income for fiscal Q1, rising 21% from the same quarter last year.

The company’s value proposition has likewise grown, taking its stock higher by approximately 25% over the last year.

However, the stock has become increasingly expensive, with a P/E ratio of 42 and a price-to-sales (P/S) ratio of 8. Even with earnings growth of over 20%, that could leave investors questioning its valuation with a recent history of single-digit revenue growth. But amid the continuing popularity of its database and software capabilities, the stock should hold its own.

Why investors might consider MongoDB

In contrast, MongoDB is comparatively new, existing only since 2007. As previously mentioned, it derives its revenue from its non-relational database, which could upend the database industry as Oracle’s traditional database model becomes outdated.

Non-relational databases stand out for their ability to store and manage data types that do not fit into an existing structure. Thus, users can store data types, such as videos or abstract text, that a more structured database would struggle to manage.

Its Atlas database has attracted more than 85 million downloads and Atlas clusters. Moreover, its community consists of over 1 million developers and many of the world’s most prominent corporations use its services.

Nonetheless, it has suffered a steep deceleration in its growth in recent quarters as fewer multiyear licensing deals, which recognize revenue up front, came due. In the second quarter of fiscal 2025 (ended July 31), revenue of $478 million rose 13% compared to the same period last year. That was below the 17% increase for fiscal 2025 and a 31% rise in the previous fiscal year.

Also, the $55 million loss in fiscal Q2 was up from the second quarter of fiscal 2024, when the company lost $38 million.

The slowing revenue growth appears to have taken its toll on the stock, down more than 20% over the last year.

As a money-losing company, it has no P/E ratio, and one has to wonder whether its P/S ratio of 12 will attract investors given its growth slowdown from last year. Considering this situation, investors may want to stay on the sidelines until they see signs of improvement.

Oracle or MongoDB?

When accounting for the state of both companies, investors should probably choose Oracle. Admittedly, MongoDB’s non-relational database could challenge Oracle’s long-standing database business over time.

However, Oracle continues to grow its software business, and its presence in the cloud should keep its AI capabilities competitive in the tech market. Additionally, Oracle turns a profit and offers a lower valuation to investors despite becoming an increasingly expensive stock.

Ultimately, unless MongoDB can address its decelerating growth, its stock is unlikely to gain traction at its current price.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Will Healy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Microsoft, MongoDB, Oracle, Salesforce, and Tencent. The Motley Fool recommends Alibaba Group and International Business Machines and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.